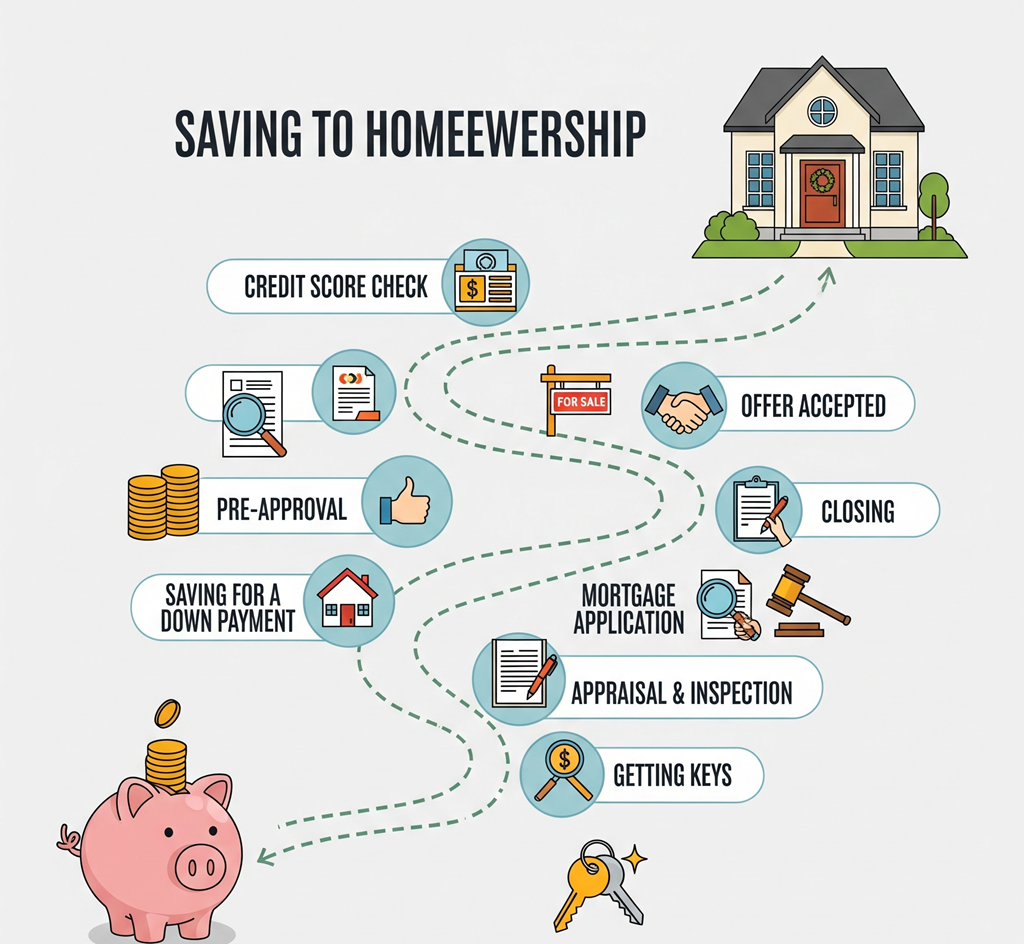

The journey to homeownership is exciting, but the mortgage process itself can often feel like a complicated and mysterious path. From initial savings goals to finally getting the keys, there are numerous steps, a lot of jargon, and critical deadlines to meet.

Understanding this timeline is the key to a smooth and stress-free experience. As we move towards the end of 2025, being well-prepared is more important than ever. This guide breaks down the entire UK mortgage application process into a clear, chronological roadmap.

Phase 1: The Preparation (3-12 Months Before You Apply)

This is the foundational stage where you build the financial strength for your application.

- Step 1: The Financial Health Check Before anything else, get a crystal-clear picture of your finances. Track your income and all your monthly outgoings to understand your saving capacity and what you can realistically afford for a mortgage payment.

- Step 2: The Credit Score Deep Dive Your credit history is one of the most important factors for any lender. Download your credit reports from all three main UK agencies (Experian, Equifax, TransUnion). Check for errors and spend these preparatory months paying down debts and improving your score wherever possible.

- Step 3: Save for Your Deposit & Costs Your deposit will be your biggest savings goal, but don’t forget the other significant costs. You will also need funds for solicitor fees, mortgage arrangement fees, survey costs, and potentially Stamp Duty Land Tax.

Phase 2: The Search (1-3 Months Before You Offer)

With your finances in good shape, you can now move into the active search phase.

- Step 4: Speak to a Mortgage Advisor This is arguably the most crucial step. Instead of using generic online calculators, an expert mortgage advisor will perform a detailed assessment of your finances to tell you exactly how much you can borrow. They provide access to the whole market, not just one bank’s products.

- Step 5: Get Your Agreement in Principle (AIP) Based on your initial assessment, your advisor will secure an AIP for you. This is an official statement from a lender confirming they are prepared to lend you a certain amount, in principle. An AIP proves to estate agents that you are a serious, credible buyer.

- Step 6: The Property Hunt Armed with your AIP and a firm budget, you can now search for your dream home with confidence.

Phase 3: The Application (The “Live” Stage)

You’ve had an offer accepted on a property. Now the formal process begins.

- Step 7: Submit the Full Mortgage Application Your mortgage advisor will now submit your full, detailed application to the chosen lender along with all your supporting documents (payslips, bank statements, proof of deposit, etc.).

- Step 8: The Lender’s Valuation The lender will arrange for a surveyor to visit the property to conduct a valuation. This is to ensure the property is worth the amount you are paying for it and provides adequate security for the loan.

- Step 9: The Underwriting Process This is where the lender’s underwriting team meticulously reviews every aspect of your file—your income, your credit history, your employment stability, and the property details—to make their final lending decision.

- Step 10: Receive Your Formal Mortgage Offer Success! The mortgage offer is the official document from the lender confirming they will provide the funds. This is a huge milestone and allows the legal process to move forward.

Phase 4: The Legal Process to Completion

With the finance secured, your solicitor or conveyancer takes the lead.

- Step 11: Conveyancing and Legal Searches Your solicitor will conduct local authority searches, check contracts, and handle all the legal aspects of transferring ownership of the property.

- Step 12: Exchange of Contracts This is the point of no return. You and the seller sign identical contracts and the deposit is paid. The deal is now legally binding.

- Step 13: Completion Day! This is the day your solicitor draws down the funds from the mortgage lender, transfers the full amount to the seller’s solicitor, and registers the sale. Once the money is confirmed as received, the keys are officially yours.

Conclusion

While the mortgage journey is detailed, it becomes far less intimidating when you see it as a series of manageable steps. The key to navigating it successfully is preparation and expert guidance. Having a professional mortgage advisor like the team at Confidence in Finance by your side from Step 4 onwards turns a complex process into a clear path to your new front door.